- Homepage /

- Blog /

- Crypto License /

- Mica Licensing Offshore Structures Study

Study: Offshore Corporate Structures with MiCA Licensing: What Nobody Thought Possible

Major exchanges kept their BVI and Cayman parents. Offshore token issuers file EU white papers without a single European entity. The regulation always allowed this. Most advisors just did not read it carefully enough.

Key Findings

- MiCA distinguishes two fundamentally different actors: CASPs, who must have a genuine EU entity, and token issuers/offerors, who do not need to incorporate in the EU to file a white paper and offer tokens to European investors.

- Of 586 token issuers in the ESMA white paper register with identifiable LEI country codes, 62% are domiciled outside the EU or EEA, including 120 BVI entities and 51 Cayman Islands entities.

- Major exchanges including Bybit, OKX, and Crypto.com operate MiCA-compliant through EU subsidiaries while their offshore parent structures remain untouched.

- ARTs and EMTs are the exception: stablecoin and asset-referenced token issuers must have an EU-incorporated issuer, with no offshore flexibility available.

Early in 2025, a crypto founder spent six months dismantling their British Virgin Islands group structure, moving IP, redomiciling the treasury, and incorporating a new parent in Ireland. Their lawyers had told them MiCA meant Europe. If you wanted to operate in the EU, you needed a European company. Full stop.

They launched in early 2026, fully licensed, fully relocated, and fully European. Then they looked at the ESMA public register.

Bybit’s global parent is incorporated in the British Virgin Islands and headquartered in Dubai. Bybit EU GmbH, its Austrian subsidiary, holds the Markets in Crypto-Assets Regulation (MiCA) license. OKX’s Seychelles entity sits at the top of a structure whose Maltese subsidiary, OKX Europe Limited, was authorized by the Malta Financial Services Authority (MFSA). Crypto.com runs global operations through Singapore, while its EU-facing entity, Foris DAX MT Limited, is a licensed Maltese crypto-asset service provider.

None of these groups relocated. All of them are MiCA-compliant. And the ESMA register shows that token issuers from the BVI, the Cayman Islands, Panama, and Singapore have been filing EU-compliant white papers since the regulation came into force, without incorporating a single EU entity.

So what does MiCA actually require? And who was wrong: the regulation, or the advisors?

Related: What’s the Difference Between EMT vs. ART in MiCA?

Is It Really Impossible to Have an Offshore Structure With a MiCA License or Token?

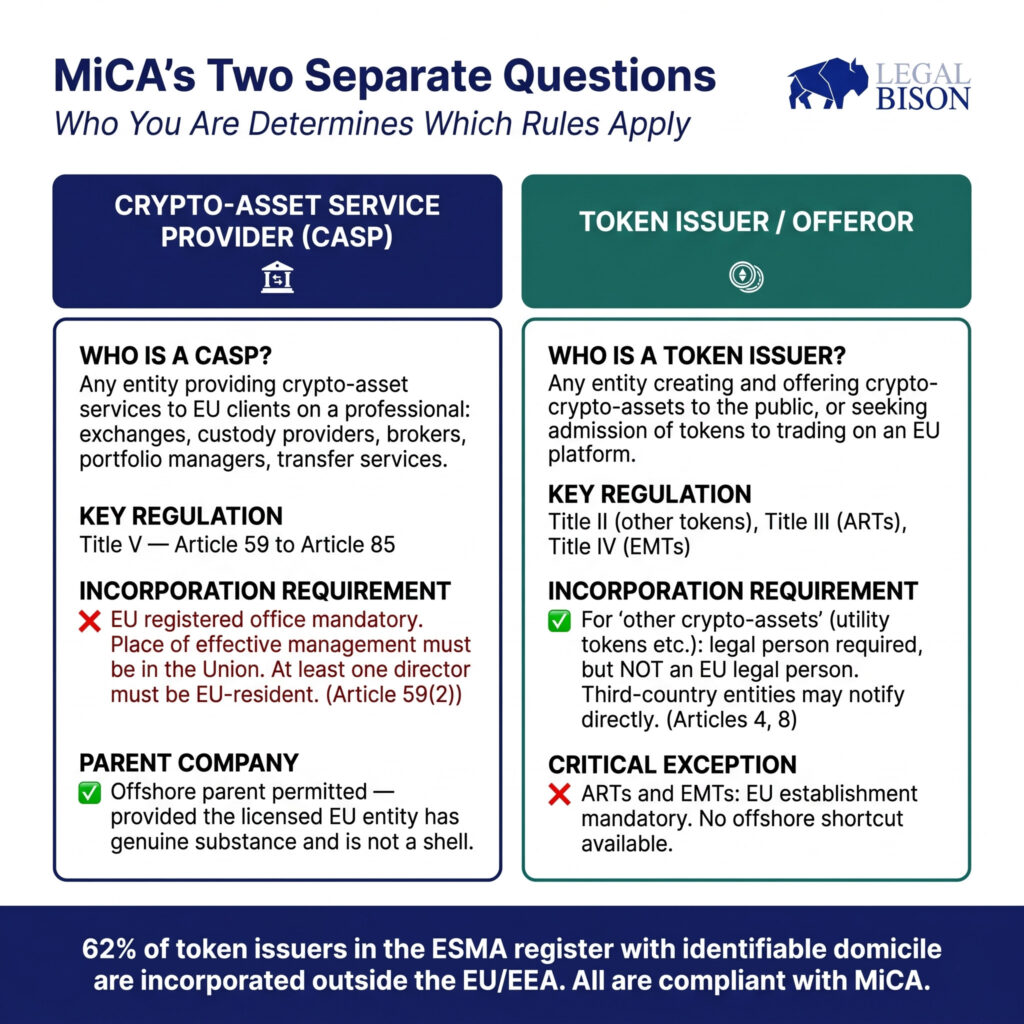

Before decoding the structural reality, it is necessary to understand that MiCA governs two fundamentally different types of actors. Conflating them is what produced the misconception.

Crypto-Asset Service Providers (CASPs) are entities whose business is providing crypto-asset services to clients on a professional basis. MiCA defines ten categories of such services in Article 3(1)(16): custody and administration of crypto-assets, operating a trading platform, exchanging crypto-assets for funds or for other crypto-assets, executing orders, placing crypto-assets, receiving and transmitting orders, providing advice, providing portfolio management, and providing transfer services. If your business model involves any of these activities directed at EU clients, you are a CASP. A centralized exchange, a custody wallet provider, a crypto broker: all CASPs, regulated under Title V of MiCA and requiring authorization under Article 59.

Token issuers and offerors are a different category entirely. These are the entities that create and offer crypto-assets to the public, or seek to have their tokens admitted to trading on an EU platform. A project launching a utility token, a layer-1 network distributing tokens at genesis, a DeFi protocol making its governance token available to European investors. All of these are token issuers or offerors, regulated under Titles II, III, and IV of MiCA, depending on the type of crypto-asset involved.

The obligations for each category are structurally different. The rules that apply to CASPs do not apply to token issuers in the same way, and vice versa.

Most of the market commentary treated them as a single question: “Does MiCA apply to you?” The correct question is two distinct ones: “Are you a CASP?” and “Are you a token issuer or offeror?” The answers determine which title of the regulation governs your situation, and critically where you need to be incorporated.

What the Regulation Actually Says

For CASPs: EU presence is mandatory

Article 59(2) of MiCA is unambiguous. A crypto-asset service provider authorized under Article 63 must have a registered office in a Member State where it carries out at least part of its crypto-asset services. The place of effective management must be in the Union. At least one director must be resident in the Union.

This part of the market assumption is correct. A BVI entity cannot obtain a CASP license. A Seychelles-incorporated exchange cannot passport into Germany as-is. The MiCA authorization is granted to the entity, and that entity must be meaningfully anchored inside the EU. There is no path around this specific requirement.

Article 68 adds the governance layer: members of the management body of a CASP must be of sufficiently good repute and possess the appropriate knowledge, skills, and experience, both individually and collectively, to perform their duties. They must be capable of committing sufficient time to effectively perform those duties. This is not a checklist formality. The National Competent Authority (NCA) conducting the authorization review assesses whether real decision-making authority sits in the EU entity or whether it is being exercised from elsewhere through a shell.

So yes, the CASP must be European. But the CASP is one entity. MiCA says nothing about where the CASP’s parent must be incorporated.

For token issuers: the picture is different

For crypto-assets other than asset-referenced tokens (ARTs) and e-money tokens (EMTs), the broad “other crypto-assets” category that covers utility tokens and most of what the market commonly calls tokens, MiCA’s white paper requirement works very differently.

Article 4(1) requires that any person making an offer to the public of such a crypto-asset in the Union must, among other things, be a legal person. Not an EU legal person. A legal person. Article 8(1) specifies that offerors and persons seeking admission to trading must notify their white paper to the competent authority of their home Member State, but then defines “home Member State” for third-country entities in Article 3(1)(33)(c): where the offeror is established in a third country, the home Member State is the Member State where the crypto-assets are intended to be offered to the public for the first time, or, at the choice of the offeror, the Member State where the first application for admission to trading is made.

In plain terms: a BVI company can notify a white paper to the Central Bank of Ireland and offer its token to European investors. It is not required to incorporate in Ireland to do so.

There is a second path under Article 5(2) and 5(3). A person seeking admission to trading and the operator of the trading platform may agree in writing that the operator will comply with the white paper requirements. When a CASP takes this on, it assumes legal responsibility for the accuracy and completeness of the disclosure. This is how exchanges like Kraken (Payward) or others have filed white papers for tokens with no centralized EU issuer. They agreed in writing to carry the obligation, and the offshore project did not need to engage an EU regulator directly.

The important exception: this structural flexibility does not extend to ARTs or EMTs. For asset-referenced tokens, Article 16 requires the issuer to be established in the Union and authorized by a competent authority. For e-money tokens, Article 48 requires the issuer to be authorized as a credit institution or electronic money institution. These categories are categorically different, and the offshore shortcut is not available for either.

Why Confusion Took Hold

Three things went wrong simultaneously.

First, the commentary collapsed two separate questions into one. “Does MiCA apply to my company?” became the framing, and the CASP substance requirements were applied as the answer to everything. Founders building token projects read about Article 59(2) and assumed it applied to them. It does not, unless they are also operating CASP services.

Second, the substance requirements for CASPs are genuinely demanding. Reading Article 68 carefully: the fit-and-proper assessment, the collective expertise requirement, the time-commitment obligations. It is easy to understand why early advisors concluded that a meaningful EU entity meant effectively moving the business to Europe. For many applicants, the internal reality of building a genuine EU management layer felt indistinguishable from a relocation.

Third, the practical challenges of early MiCA implementation reinforced caution. Some NCAs in late 2024 and early 2025 scrutinized CASP applicants with heavily outsourced operations, and the industry absorbed this as a signal that offshore structures were unwelcome. The signal was more specific than that: hollow EU entities with no genuine local substance were unwelcome. That is meaningfully different from saying offshore parents are prohibited.

Token Issuers Offshore: What the Register Shows

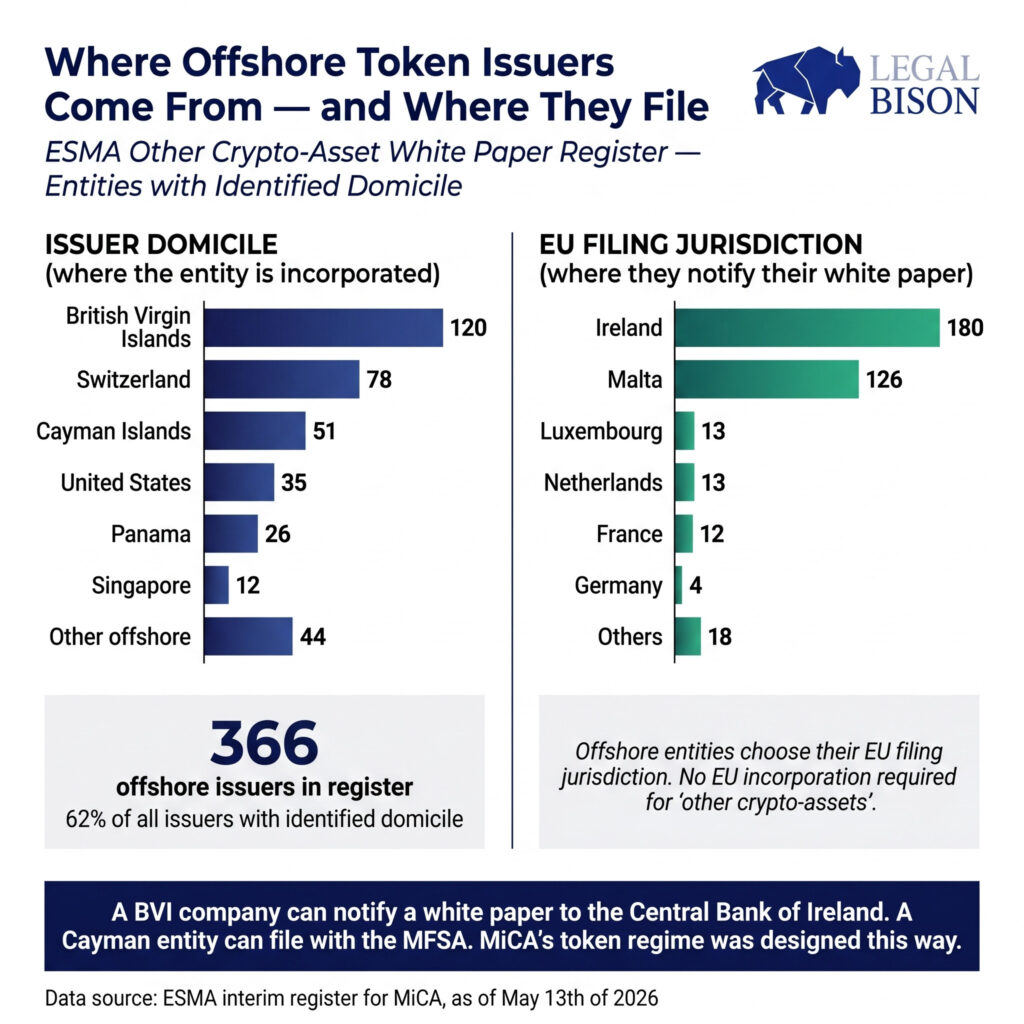

The ESMA public register of white papers for crypto-assets other than ARTs and EMTs settles the question empirically. Of the 586 token issuers in that register with identifiable Legal Entity Identifier (LEI) country codes, 366 (62%) are domiciled outside the EU or EEA.

The geography is striking. 120 entities are incorporated in the British Virgin Islands. 78 are in Switzerland. 51 are in the Cayman Islands. 26 are in Panama. 35 are incorporated in the United States.

These entities chose their EU filing jurisdictions deliberately. Ireland received white paper notifications from 180 offshore issuers. Malta received 126. Luxembourg and the Netherlands each received around 13. BVI-incorporated entities alone filed 68 white papers in Ireland and 33 in Malta.

The names in the register are not obscure projects. Gensyn Network Ltd, a BVI company, filed its white paper in France. Nexus Sub (BVI) Limited filed in France, with Payward Global Solutions (Kraken’s entity) listed as the CASP taking on the white paper obligation. The Horizen Foundation, incorporated in the Cayman Islands, filed in Germany. zkVerify Foundation, also Cayman-based, similarly filed in Germany. Init Capital Ltd, a BVI entity, filed in Ireland.

None of these required an EU incorporation. The regulation provided the path directly.

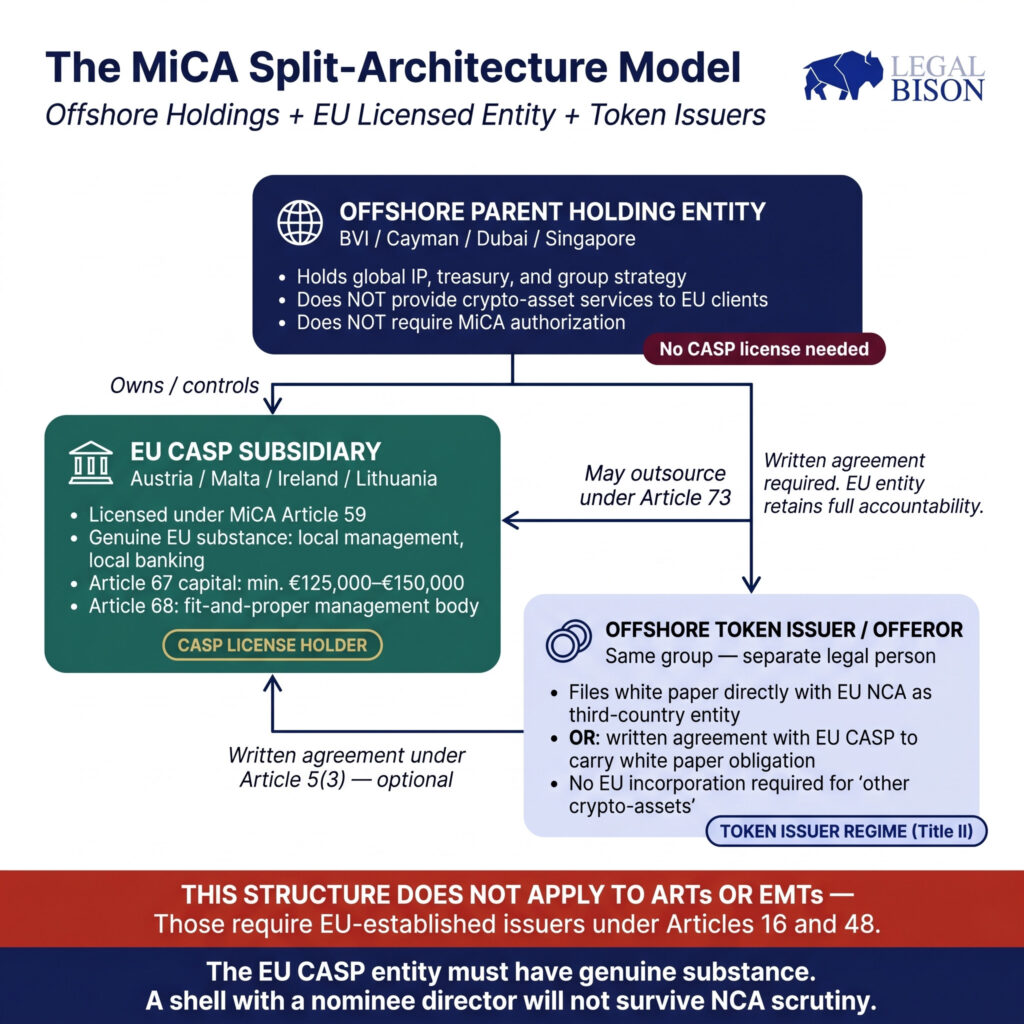

The Split-Architecture Model: How It Works in Practice

The architecture that major exchanges use follows a clear logic. Understanding it in sequence is useful.

At the top sits an offshore holding entity. This is where the group’s global treasury, intellectual property ownership, and strategic functions typically reside. The holding entity does not provide crypto-asset services to EU clients. It does not hold a CASP license. It does not need one.

Below it, an EU operational subsidiary is incorporated in a Member State with a functioning MiCA licensing pipeline: Austria, Malta, Ireland, and Lithuania have processed meaningful volumes. This subsidiary is the licensed CASP. It employs local management. It maintains local banking relationships. Its management body meets the Article 68 suitability requirements. Its paid-in capital satisfies the Article 67 thresholds: at minimum EUR 125,000 for entities providing custody or exchange services, or EUR 150,000 if operating a trading platform. The place of effective management is genuinely in the EU, and can withstand regulatory scrutiny, because the EU entity’s management actually runs the EU operations.

The relationship between the offshore parent and the EU CASP is governed by the outsourcing framework under Article 73. The EU CASP can outsource operational functions to the parent or to group affiliates, but it must retain the expertise to evaluate the quality of those services and supervise them effectively. It must have direct access to the relevant information of outsourced services. Responsibility cannot be delegated. The EU CASP remains fully accountable to its NCA for everything it outsources. If the parent provides technology infrastructure, the EU entity cannot simply abdicate oversight of it. The outsourcing agreement must be in writing, must give the CASP the right to terminate, and must ensure that the parent cooperates with the NCA’s supervisory functions.

In practice, this means the EU entity needs more than a registered address and a nominee director. It needs people who genuinely manage the EU operations, who can produce documentation and present to regulators, and who understand what the parent is providing on its behalf. The structural separation between parent and subsidiary is real, but the EU entity must have the internal capability to be held accountable for the group relationship.

Token issuers in the same group have a third structural option alongside the two already described. Where the project is not providing CASP services itself, the offshore token entity can file its own white paper with an EU competent authority as described above. Alternatively, if the group’s EU CASP operates a trading platform, that entity can take on the white paper obligation by written agreement under Article 5(3), effectively serving as the regulatory interface for the offshore token entity without the token entity needing any EU presence at all.

What the Architecture Cannot Do

Three things remain outside the reach of any offshore-parent structure, and founders who miss them expose themselves to serious regulatory risk.

The EU entity cannot be a shell. This is the boundary that several early MiCA applicants discovered the hard way. A nominee director arrangement, where decisions are effectively made from the offshore parent and the EU director signs off on instructions from abroad, fails Article 59(2) and the genuine substance test that regulators apply to Article 68. Some NCAs now conduct live interviews with management body members as a standard part of the fit-and-proper assessment. They ask probing questions about governance, risk management, and operational authority. A director who cannot speak credibly about the EU entity’s actual operations is a director who will not pass the review.

The offshore parent cannot solicit EU clients. Article 61 provides a carve-out for services provided to EU clients at their own exclusive initiative. ESMA’s guidelines on reverse solicitation, published under the mandate of Article 61(3), define the outer boundary of this exemption in narrow terms. A firm that maintains a website in Hungarian or Czech or Lithuanian, runs affiliate programs generating EU signups, or participates in EU-facing marketing through any channel, regardless of whether that activity comes from the offshore parent or an entity acting on its behalf, is not benefiting from the reverse solicitation exemption. The offshore parent of a licensed EU CASP cannot conduct parallel solicitation of EU users and claim its EU subsidiary handles the regulated portion. Regulators will look at the commercial reality of how clients are acquired, not the internal organizational chart.

ARTs and EMTs require EU issuers, full stop. Any project planning to issue a stablecoin or asset-referenced token should treat Articles 16 and 48 as the starting point for their structure, not the CASP regime. The offshore flexibility available for utility tokens and similar assets does not apply here, and attempting to apply it through a proxy structure will not survive regulatory review.

To Conclude

For CASP operators: The offshore holding can stay offshore. The question is not whether to relocate the parent, but whether the EU subsidiary has genuine substance: management that actually runs the EU operations, capital that meets the Article 67 thresholds, governance that satisfies Article 68, and an outsourcing framework with the parent that does not hollow out the EU entity’s accountability. Jurisdiction selection for the EU subsidiary matters: Austria, Malta, Ireland, and Lithuania each offer functioning licensing pipelines and different regulatory cultures that suit different business models.

For token issuers: If you are not providing CASP services, you do not need an EU entity to file a white paper and offer your token to European investors. A BVI or Cayman company can notify the Central Bank of Ireland or the MFSA and proceed. If your token is already listed on a licensed EU exchange, that exchange may be willing to take on the white paper obligation by written agreement, in which case your regulatory burden for EU market access is reduced further. The practical choice of filing jurisdiction still matters. Ireland has processed the broadest range of token categories, while Malta has deeper infrastructure for crypto-specific compliance work.

For hybrid structures: Groups that both issue tokens and provide CASP services need to map each activity to its regulatory regime separately. The token issuer entity and the CASP entity may be different legal persons within the same group. Their obligations do not cross over simply because they share an ultimate parent. This structural separation can be a feature, not a complication: the offshore token treasury operates under the token issuer regime, the EU CASP operates under Title V, and the offshore parent holds the group together without itself needing authorization.

The founders who relocated in 2025 were not necessarily wrong to do so. A consolidated EU presence has operational advantages, and a genuinely EU-anchored group is simpler to manage from a regulatory standpoint. But they acted on an assumption about what MiCA required that the regulation itself does not fully support. The register makes this visible. The architecture of MiCA was always capable of accommodating offshore parent structures, provided the entity that actually serves EU clients is genuinely present, genuinely managed, and genuinely accountable inside the Union.

Key Takeaways

- The offshore holding can stay offshore. MiCA requires the EU-facing CASP subsidiary to have genuine substance, not the parent to relocate.

- Token issuers without CASP activities do not need an EU entity. A BVI or Cayman company can notify a white paper directly to an EU competent authority and offer tokens to European investors.

- The EU subsidiary cannot be a shell. Nominee director arrangements fail the Article 59(2) substance test. NCAs conduct live interviews and assess whether real decision-making authority genuinely sits inside the EU entity.

- The offshore parent cannot solicit EU clients. ESMA’s reverse solicitation guidelines are narrow. Any EU-directed marketing, regardless of whether it comes from the parent or an affiliate, removes the exemption.

- ARTs and EMTs require EU issuers, full stop. The offshore flexibility available for utility tokens does not extend to stablecoins or asset-referenced tokens.