- Homepage /

- Blog /

- Crypto License /

- Mica White Paper Legal Filing

Study: The MiCA White Paper Is a Legal Filing, Not a Marketing Document

The MiCA white paper serves as a mandatory legal disclosure instrument rather than a narrative marketing pitch. Its legal function is equivalent to a traditional finance securities prospectus. This study by LegalBison analyses the transition from narrative-driven crypto documentation to the mandatory legal disclosure instruments now required in the European Union.

Key Findings

- Under MiCA, a white paper is a mandatory legal disclosure instrument, not a narrative pitch. Its closest analogue in traditional finance is a securities prospectus.

- Commission Implementing Regulation (EU) 2024/2984 requires white papers to be submitted in a structured digital format so that automated cross-border analysis can run identically on every filing.

- MiCA draws three distinct token categories: OTHER (utility tokens and most general crypto-assets), ART (asset-referenced tokens), and EMT (electronic money tokens). Each carries different white paper requirements, different authorized preparers, and different liability rules.

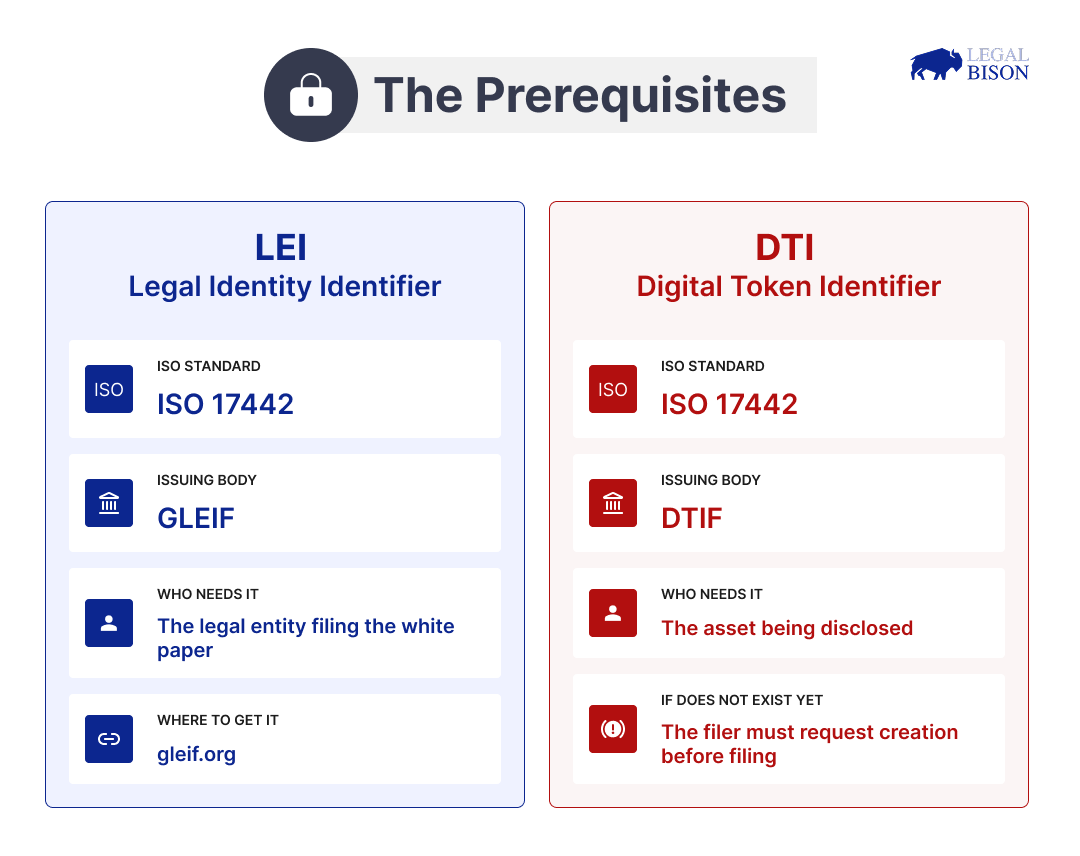

- Two mandatory identifiers, the Legal Entity Identifier (LEI) and the Digital Token Identifier (DTI), must be in place before white paper preparation begins. Projects that reach the filing stage without both codes face a full restart.

- ESMA’s automated validation system runs 257 existence checks and 223 value checks. A filing that fails an Error-level assertion does not reach a human reviewer.

- Content accuracy and technical validity are two separate obligations. Both rest with the filing party.

Background: Why This Study Matters

Most people working in crypto still associate the term white paper with the document type that defined the ICO era: a narrative piece designed to explain a project and attract buyers. MiCA replaced that concept with something categorically different, and the gap between the popular understanding and the legal reality is where many compliance failures begin.

This study, drawn from the sixth installment of the MiCA Decoded series co-authored by LegalBison’s Co-Founding and Managing Directors, sets out what the MiCA white paper actually is, who is responsible for it, and what the technical filing process requires. The purpose is to give founders a clear picture of what they are entering before they start preparing documentation.

Related: Why the Regulator Sees Your Compliance Team as a Single Brain

What a MiCA White Paper Actually Is

The MiCA white paper is a legal filing with machine-enforced standards. That sentence is the entire summary, and everything that follows explains what it means in practice.

Under Commission Implementing Regulation (EU) 2024/2984, the document must be prepared in a structured digital format designed for automated cross-border comparability. ESMA and all national competent authorities across every EU member state run identical automated checks on every submission. The structure is not optional. A white paper that cannot be read by the same system as every other EU filing is non-compliant, whatever its content says.

ESMA published the required taxonomy on 5 August 2025. The rules apply as of 23 December 2025.

Three token categories fall under MiCA, each with its own white paper template:

OTHER tokens cover the majority of what is currently in the market: utility tokens, general crypto-assets, and anything that does not qualify as an ART or EMT. The obligation to prepare the white paper falls on the offeror, the person seeking admission to trading, or a CASP operating a trading platform that takes on the responsibility by written agreement.

ART (Asset-Referenced Tokens) reference a basket of assets rather than a single currency. Only authorized issuers or credit institutions can prepare the white paper. Strict civil liability extends to members of the issuer’s administrative, management, or supervisory body.

EMT (Electronic Money Tokens) are single-currency pegged tokens. Only licensed electronic money institutions or credit institutions can issue them, and the same strict liability framework applies.

The asset’s characteristics determine which category it falls into. The project does not choose.

Who Carries the Obligation (and the Liability)

For the vast majority of tokens currently in the market (the OTHER category), the legal obligation belongs to the offeror or the person seeking admission to trading. This does not automatically mean the entity that originally created the token.

A practical consequence for offshore-incorporated projects: a BVI foundation or Cayman entity can be the offeror under MiCA and carry the white paper obligation directly, without relocating its legal seat to Europe. The ESMA registers confirm this is standard practice. The majority of independent white paper filings come from entities headquartered outside the EU.

A CASP operating a trading platform can also take on the white paper obligation, either on its own initiative or by written agreement with the project team. When a CASP files, it assumes legal responsibility for accuracy and completeness. However, this does not eliminate the project’s own exposure. Under MiCA Article 14(3), the original person seeking admission to trading remains legally responsible if they provide incomplete, unfair, unclear, or misleading information to the CASP. Filing responsibility can be delegated. Liability cannot be fully transferred.

For ARTs and EMTs, the liability framework is stricter. Strict civil liability for the white paper explicitly extends to members of the administrative, management, or supervisory body of the issuer. Any contractual attempt to limit or exclude that liability is legally void.

Related: “We Have an EU Office” Is Not Enough: Here’s What MiCA Regulators Actually Want to See

Two Prerequisites Before Writing Begins

Two mandatory identifiers must be secured before white paper preparation starts. Missing either at the submission stage means the entire process restarts.

The Legal Entity Identifier (LEI) is an ISO 17442 code assigned to legal entities, maintained in the Global LEI database administered by GLEIF. Article 3 of Commission Delegated Regulation (EU) 2025/421 requires that all white paper preparers identify their own legal entity with a valid LEI code. For entities that do not already hold one, the application must be completed first.

The Digital Token Identifier (DTI) is an ISO 24165 code that identifies the crypto-asset itself, maintained in the DTIF registry. If the DTI does not yet exist for the asset, someone must request its creation from the DTIF before the white paper can be submitted. Where a CASP is filing for an asset with no centralized issuer and no existing white paper, the platform is responsible for retrieving or requesting the DTI directly.

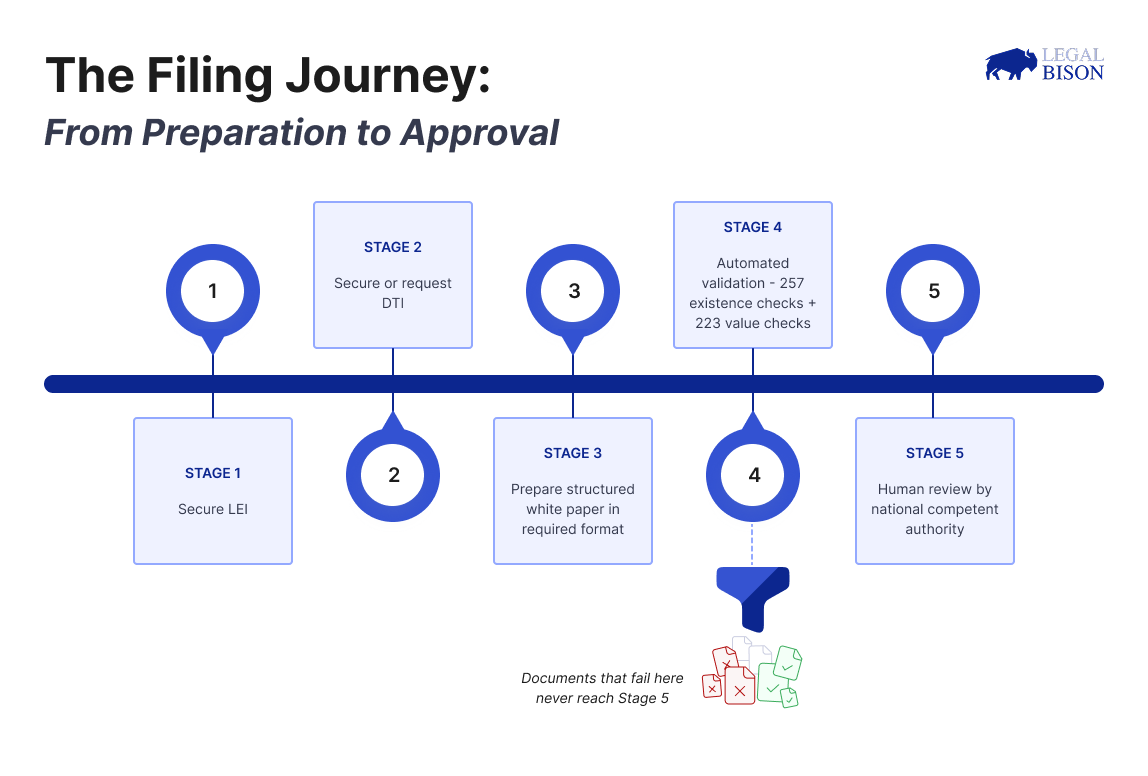

How the Automated Gate Works

No human at a national competent authority reviews a white paper that fails automated checks. The ESMA taxonomy defines 257 existence checks, which verify that required fields are present, and 223 value checks, which verify that field content is valid. A filing that fails an Error-level assertion does not proceed.

Several specific technical requirements follow from this structure:

Projects offering tokens in multiple EU member states must submit each language version of the white paper as a separately structured file. All language versions must be identically organized at the field level. A translation that does not mirror the source structure is technically non-compliant regardless of its linguistic accuracy.

Sustainability disclosures carry specific unit requirements. Energy consumption must be reported in kWh; CO2 emissions must be reported in tCO2. These are legal disclosure fields, not optional environmental reporting. Filings using different units or omitting the fields trigger a validation failure.

The pattern across every one of these requirements is the same. Technical validity and content accuracy are separate obligations. Legal review covers the content. Technical structuring covers the format. Both rest with the filing party. A perfectly drafted legal disclosure in the wrong structure fails. A structurally valid file with misleading content also fails, at a different stage and with different consequences.

Related: Thinking a CASP License Covers Payments, Perps or Futures is a Major Mistake

What This Means for Founders

MiCA did not adjust the existing concept of a crypto white paper, but replaced it with a different instrument that happens to share the name.

The filing is a legal document with mandatory identifiers, structured format requirements designed for automated cross-border comparability, and named personal liability attached to whoever signs off on it. The entry gate to the European crypto market for most token projects runs through it.

Projects that treat white paper preparation as a document-writing exercise will encounter automated enforcement before they reach a human regulator. Projects that approach it as a compliance process, beginning with LEI and DTI acquisition, confirming which token category applies, and building the structured filing to match the ESMA taxonomy, are positioned to clear the automated gate and have their submission reviewed on its merits.

LegalBison advises crypto and FinTech companies on MiCA licensing, CASP authorization, token structuring, and regulatory compliance across the EU and beyond. This article is for informational purposes only and does not constitute legal advice.